May 29, 2025

Transform 10-Ks into instant insights. CompuText extracts key events, sentiment & drivers from filings—no more sifting through boilerplate.

Uncover how Context Analytics' real-time consensus sentiment reports help traders spot alpha by aligning signals from Twitter, Stocktwits & News.

Context Analytics combines Twitter-based sentiment data with momentum indicators in a machine learning model to predict stock returns and outperform the S&P 500 using the S-Factor Feed.

Discover market-moving insights before they hit the headlines with Context Analytics' Emerging Topics Data Feed — an AI-powered tool that tracks real-time financial trends on Twitter to give investors a decisive edge.

April 16, 2025

In 2025, a single tweet briefly added trillions to the market—before vanishing just as fast. Discover how real-time sentiment and tools like ThemeX from Context Analytics help investors detect, respond to, and manage market-moving misinformation in milliseconds.

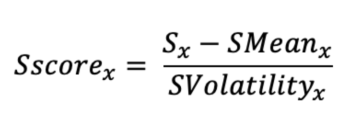

In a volatile start to 2025, Context Analytics’ Twitter-based S-Score has remained a reliable sentiment signal—powering a long-short strategy that’s outperformed SPY by nearly 20% year-to-date. Discover how social sentiment is helping traders navigate chaos with clarity.

March 27, 2025

In today’s volatile market, understanding how themes like tariffs and trade wars impact companies is essential. Context Analytics’ ThemeXplorer tool uncovers real-time trends in SEC filings and earnings calls, helping investors identify risk exposure and sector impact fast.

Context Analytics has expanded its social sentiment coverage to include Australian securities (ASX), using Twitter data and proprietary NLP technology to generate actionable trades.

Policy shifts by DOGE present challenges for companies. ThemeX equips risk managers with the tools to monitor and analyze these changes in real time.

February 28, 2025

2024 was an exceptional year for the market, with the S&P 500 rising more than 24%, and that momentum has carried over into 2025, where the index is already up over 4% year-to-date. The purpose of this blog is to illustrate how our data is performing while the market is off to such a strong start.

February 28, 2025

Sentiment data can be used for global trading strategies. Our approach outperforms the NSE NIFTY50 baseline using S-Score and S-Volume.

February 13, 2025

CA's Advanced Parsing Engine and Twitter Source Rating Algorithm can be leveraged to improve retrieval accuracy and overall performance for LLM inputs.

January 31, 2025

Compare the current OpenAI integration in our Unstructured Data Terminal with a locally run version of DeepSeek-R1—Distill Qwen 7B—using a relevant financial document example: the Tesla 10-Q report from 04/24/2024. By examining these models’ responses side by side, we aim to find out whether DeepSeek’s cost-efficient and open-sourced prowess genuinely disrupts the landscape—or if it remains just another intriguing entry in the LLM marketplace.

Last year Context Analytics (CA) released a news sentiment data feed. This paper will explore an index created with CA sentiment data compared to the S&P 500 RavenPack AI Sentiment Index (Bloomberg ticker: CSRPAISE). Both use news-based sentiment data to construct a sentiment-driven, sector-based index. The objectives of this research is to isolate and evaluate the performance of Context Analytics' news sentiment as a long-term predictor, applying a methodology comparable to the benchmark index.

Learn how Context Analytics uses Twitter sentiment with the S-Factor Feed to power a Monthly Long-Only Strategy that consistently outperforms the S&P 500.

November 21, 2024

What if you could spot a bullish trend before it takes off? Context Analytics has created a long-term cryptocurrency signal using social sentiment from Twitter messages on all cryptocurrencies, and it may be the solution.

November 20, 2024

This week’s blog explores how Twitter volume can serve as a predictive signal for Bitcoin’s weekly returns, focusing on an engineered volume metric that captures the macro-level cryptocurrency conversation.

November 6, 2024

In the blog, we focus on the Russell 3000 universe, using CompuText data on 8-K filings from 2014 onward. Identifying key language in these filings with CompuText can reveal indicators of subsequent market movement.

October 31, 2024

The Quantitative News Feed is a predictive news sentiment tool useful for trading strategy building and risk management. In previous research, our focus centered on shorter-term sentiment — specifically, a 24-hour positivity ratio for companies based on news sentiment. This was calculated as the ratio of aggregate positive mentions to total indicative sentiment hits. In this study, however, we extend our approach to look at sentiment trends over a 30-day period.

October 9, 2024

Dive into an analysis of the Futures market, leveraging sentiment insights from our feed to uncover actionable trading strategies.

Context Analytics’ S-Factor feed can be used to generate alpha. Whether you’re analyzing sentiment or shifts in sentiment, CA’s tools provide a granular view of social sentiment, helping investors capture opportunities that traditional data sources might miss. In today’s fast-moving markets, understanding how sentiment is trending—rather than just where it stands—can give traders and investors a significant edge. With the Twitter S-Factor feed, CA empowers its clients to stay ahead of the curve, turning sentiment data into actionable signals for superior performance

September 25, 2024

We conducted an analysis on the Russell 3000 universe using Computext extractions over a period starting from the beginning of 2014, encompassing over ten years of data. The goal was to assess the long-term impact of the sentiment extracted from these government filings.

September 11, 2024

Combining these three data sources—Twitter, Stocktwits, and News—can enhance trading signals. Specifically, in this blog, we examine the sentiment for individual securities across all three platforms.

September 4, 2024

In this blog, we introduce a Weighted Average Sentiment signal, specifically designed to predict short-term returns. The signal is constructed using two key metrics from our data feed: Average Sentiment and Word Count of news articles.

August 28, 2024

We developed a long-short trading strategy that uses a metric which reflects both sentiment and volume, providing a reliable indicator of market momentum and helping us identify entry and exit points for trades.

August 22, 2024

Highly positive news can be a useful indicator for identifying overnight risers, while highly negative news can help spot potential declines.

August 7, 2024

The COVID-19 pandemic has significantly increased the use of online forums, including Reddit, for discussing stock market predictions and rallying around certain securities. This phenomenon has given rise to a rallying effect, where collective enthusiasm or concern about a stock can drive its price movement. One of the most notable examples of this effect was the GameStop (GME) saga, where a Reddit user known as Roaring Kitty played a pivotal role in rallying retail investors to drive up the stock's price.

Context Analytics’ Quantitative News Feed is a powerful tool for quantitative strategies and alpha generation, offering predictive news sentiment. The purpose of this research is to explore the effect of prolonged news attention on subsequent intermediate market performance.

July 17, 2024

Today, we are proud to officially announce our newest product: Computext. Computext searches through filings from both domestic and international companies, tagging relevant sentences for specific financial topics.

At Context Analytics, we have extensively researched how sentiment regarding individual securities can predict price movements. In this research, we aim to determine if the network of securities tagged together can enhance our predictive signals.

June 27, 2024

Overnight trading occurs between market close to the opening of the next day’s trading session. This period is often volatile due to factors such as international market movements, geopolitical events, and company-specific news, which can cause significant price movements and result in gaps up or down at market open.

June 5, 2024

Previously, our research utilized raw calculated scores or standardized scores, focusing on average and summated sentiment. In this blog, we explore the use of additional metrics from our feed. Our research indicates that the Negativity Ratio is a predictive metric for future returns. By extending the analysis to more extreme groupings (deciles and ventiles), we uncover more pronounced return differentials, with the top ventile group even outperforming the S&P 500.

Twitter sentiment can be leveraged to enhance traditional trading strategies. By integrating sentiment analysis with overnight momentum, traders can gain a more nuanced understanding of market movements and potentially achieve better returns.

As Twitter relative volume increases, the signals derived from sentiment analysis become more pronounced, especially for extreme negative sentiment signals. This research provides another method to leverage social sentiment data for robust trading signals, offering valuable insights for traders and risk analysts alike.

May 21, 2024

UDP provides a sophisticated dashboard consolidating all aspects of a pitch deck into a comprehensive, easy-to-navigate view. The dashboard is designed with three main components, each addressing critical pain points in the VC firm's pitch deck evaluation process: Company Overview and Summary Feature, Document Curated GPT, and Time Series Data Extraction and Visualization.

May 14, 2024

Known for his pivotal role in the 2021 GameStop stock saga, Roaring Kitty once again captured the internet's attention. Back then, he led a vast online community to buy these stocks, causing their prices to skyrocket in a dramatic move against hedge funds that were shorting them. On Sunday Night, Roaring Kitty posted again, sparking a similar chain reaction.

May 8, 2024

In this blog, we delve into the analysis of news fluctuations for companies and their repercussions on price movements. Our approach was to create a metric called the Delta S-Score, which serves as a key indicator of changes in news sentiment prior to market open. By quantifying these changes, we aimed to discern their influence on subsequent stock returns.

Exploration into Bayesian Probability has yielded promising results, confirming its role in enhancing signal predictability. By refining methodologies and leveraging Context Analytics social sentiment data, we continue to uncover opportunities for stock market returns.

April 24, 2024

Our strategy is simple: we take a long position in the top 5 ETFs – representing the most positively discussed ETFs on StockTwits – and a short position in the bottom 5 ETFs – representing the most negatively discussed.When conversation volume increases on StockTwits, the corresponding sentiment can serve as a valuable predictor of market trends.

Our previous research has suggested a correlation between news sentiment surrounding companies and price movements. In this blog, we introduce novel standardized metric designed to serve as a signal for traders.

April 10, 2024

In this blog, we explore the application of the Twitter S-Score in monitoring pre-Earnings Call discussions about companies.

While our news feed encompasses over 4,000 unique companies, for this research, we narrowed our focus to S&P 500 companies. Our objective was to examine the impact of extreme news days on the stock market.

March 28, 2024

Securities with extremely positive sentiment we expect to outperform the market, while with securities with extremely negative sentiment we expect to underperform. This blog demonstrates a pattern between the S-Score and the subsequent Open-to-Close return period.

Furthering our Negativity Percentage research, we looked at year-to-date data, compared to the initial findings that suggested a correlation: companies with higher negativity ratios in their language tended to underperform in the market.

March 13, 2024

This blog aims to focus on overnight price movements and demonstrate how the S-Score from Context Analytics can assist in managing risk associated with overnight positions. Such insights could prove invaluable for risk analysts, enabling them to monitor which securities are experiencing negative conversations on Twitter leading up to the market close.

Our Stocktwits data can be effectively leveraged with various techniques such as the Bayesian Accuracy Rating (BAR).

February 28, 2024

Following our initial research on Context Analytics’ Quantitative News Feed sentiment with daily close-to-close returns, we conducted a follow-up study to evaluate its effectiveness so far in 2024.

February 21, 2024

The News Widget enhancement on the UDT enables users to access breaking news, market updates, and relevant articles directly within the UDT dashboard, eliminating the need to switch between multiple platforms or sources.

February 14, 2024

This case study demonstrates a unique use case of not only selecting securities but also weighting them based on news sentiment. By aggregating news metrics and leveraging extended positive sentiment, we observe predictive power for longer-term excess returns.

February 7, 2024

Our newest data source: News Articles. We analyze and score news articles, producing sentiment metrics that are usable in trading decisions.

January 31, 2024

Many other blogs have demonstrated the predictive power of S-Score, but here we look at a derivative combination factors that can be used for daily trading. With this dataset, users can harness the power of social media in financial markets.

David Portnoy, the founder of Barstool Sports, took to Twitter to influence the stock market. This blog aims to analyze the profound impact of Portnoy's tweets on the subsequent surge in social sentiment and the movement of Spirit Airlines' stock $SAVE.

January 17, 2024

Explore the commodities markets and delve into the role of sentiment analysis on the StockTwits platform in influencing trading decisions. Our research indicates that monitoring extreme positive sentiment on StockTwits can be a valuable tool for futures traders.

January 10, 2024

Context Analytics’ S-Factor feed is the company’s most mature product. Our offering of 10+ years of out-of-sample data and a suite of sentiment factors makes this dataset unique and ideal for backtesting. With this dataset, users can harness the power of social media in financial markets.

December 21, 2023

Happy Holidays! As 2023 comes to an end, we want to reflect on all that we accomplished this year with a quick summary. We hope that 2024 will be just as exciting and productive as 2023! A huge thank you to all of our partners and customers for making it such an amazing year. Cheers!

December 13, 2023

Delve into the intricate details of the correlation between SV-Score and Crypto Returns. The SV-Score offers a valuable tool for market participants seeking to capitalize on the connection between online chatter and cryptocurrency returns

December 6, 2023

Using Social Sentiment from Twitter messages can enhance security selection. Aggregating raw sentiment over monthly periods can be used to create portfolios that outperform industry benchmarks by over 3% annually.

November 29, 2023

The UDT innovative platform is designed to enhance the flow of information from unique sources, providing a comprehensive view for users seeking valuable insights. This blog aims to delve into the various features and tools offered by the UDT, showcasing how it significantly enhances daily market intelligence.

November 20, 2023

Beginning Friday, 11/17/23, alerts triggered on abnormally high volume for OpenAI. These alerts showed an abnormally high volume for the topic. This was in response to the Tweet below, which is a statement by the OpenAI board, which explains CEO Sam Altman has departed the company.

November 15, 2023

CAPE parses financial metrics in a wide range of unique PDF formats. When dealing with a large volume of PDFs or PowerPoint slides, manually sifting through all these metrics and comparing them can be a time-consuming endeavor. CAPE saves time to spend more time on analysis and move faster than competitors.

November 8, 2023

Messages from Twitter provide useful information for security selection. Aggregating these messages and creating social sentiment scores can yield insights. Using Context Analytics Twitter S-Buzz score, customers can create portfolios that outperform the market.

November 1, 2023

The UDT's Press Release Widget allows users to sort and filter information based on the negativity percentage. This capability can be a vital tool for investors and analysts to stay ahead of market events and mitigate risk. By monitoring the negativity ratio and the number of hits, and cross-referencing with other tools like ThemeX, investors can identify potentially market-moving events early on, allowing for informed decisions.

October 18, 2023

United States defense and military weapons manufacturers are publicly traded companies. Consequently, when global tensions escalate securities in this sector become more volatile and followed. Several defense stocks have seen an uptick in value due to current Middle East tensions.

October 12, 2023

Context Analytics’ S-Factor feed is the company’s most mature product. Our offering of 10+ years of sample data and 15 different sentiment factors makes this dataset unique and ideal for back testing. With this dataset, users can harness the power of social media in financial markets.

October 4, 2023

As a follow-up to last week's 8-K Negativity Percentage blog last week, we developed a threshold strategy utilizing the Negativity Percentage. Instead of categorizing companies into tertiles, we employed a static threshold of 60% to identify companies with exceedingly negative filings. We found there is a correlation between negative 8-K filings and subsequent poor market performance.

September 28, 2023

An 8-K filing is a report filed by publicly traded companies with the U.S. Securities and Exchange Commission (SEC) to announce significant events or material information. They often contain negative news decision-makers need to react swiftly. In this blog, we explore the importance of 8-K filings, the potential negative information they can contain, and the significance of analyzing them for risk assessment.

September 20, 2023

CAPE serves as a powerful tool that transforms financial pitch decks into easily machine-readable data. Through standardization and centralization, CAPE enables swift analysis, allowing investors to dedicate more time to identifying promising investment opportunities.

September 13, 2023

Within the Context Analytics Unstructured Data Terminal, ThemeX allows users to uncover critical insights from government filings, including our recent findings on the phrase “Accepted Resignation”. Our analysis reveals a clear and significant negative correlation between the phrase and short-term returns.

September 7, 2023

Social Sentiment can be leveraged to enhance stock selection and identify price movements. Using metrics from Context Analytics, customers can utilize metrics like S-Score and S-Buzz to create strategies with reduced risk.

August 31, 2023

Context Analytics' S-Factor feed is a suite of metrics that describe Social Sentiment from messages on a social media platform separated by source. With this dataset, users can harness the power of social media in financial markets.

August 24, 2023

As the cryptocurrency market matures, Context Analytics provides a way for traders to harness sentiment and make well-informed decisions, ultimately enhancing their success in this domain.

August 21, 2023

Context Analytics' Unstructured Data Terminal (UDT) has the potential to recognize risks and facilitate swift responses to such dire events in the future. This case study examines what we found regarding the devastating wildfires that spread through Maui, more specifically Hawaiian Electric Industries (HEI). The events of the wildfires unveil numerous layers that can be analyzed through UDT. The UDT can be a helpful tool in aiding decision-makers and risk assessors in comprehensively navigating ongoing crises.

August 16, 2023

Context Analytics investigates blending the Twitter and StockTwits S-Score into one metric for trading. With this dataset, users can harness the power of social media in financial markets.

August 9, 2023

Twitter can be leveraged to enhance stock selection and identify intraday price movements. A more extreme S-Score threshold can improve portfolio returns too.

August 2, 2023

Explore the behavior of the real estate market using sentiment metrics from Context Analytics. By analyzing sentiment from StockTwits, the study identifies negative days and employs a strategy to enhance index performance.

StockTwits is a social media platform primarily focused on financial discussions and market-related topics. As a social media platform focused on investing and trading discussions, it provides a wealth of user-generated content expressing opinions, emotions, and sentiments related to various stocks and assets. By analyzing the messages and interactions on Stocktwits, sentiment analysis tools can gauge the overall mood and sentiment surrounding specific stocks or financial instruments. This information can be valuable for traders and investors seeking to understand market trends, shifts in sentiment, and potential market reactions.

July 12, 2023

Context Analytics works with brokerage firms to bring the uncorrelated and predictive power of social media to their customers. For this blog we will explore the CA widget implementation for Lightspeed Trader.

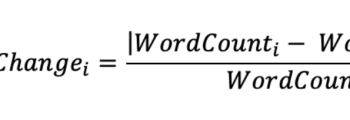

By examining the Magnitude of Word Count Percentage Change metric, investors can gain a deeper understanding of a company's potential risks. The research findings indicate that companies with fewer changes in their risk sections tend to outperform the market, while those with more changes underperform compared to the overall market.

June 21, 2023

Context Analytics’ Social Sentiment has been predictive over the last 10+ years. This blog explores the monotonic relationship between Social Sentiment and subsequent price action on US Equities.

June 15, 2023

Social Sentiment from Twitter can be used over multiple trading horizons. Using aggregations of Tweet sentiment from the previous 5 market days is predictive of weekly returns. A Long only portfolio using weekly raw sentiment outperforms the S&P 500 by 4.5% annually over the 5+ year period.

June 6, 2023

The SEC's lawsuit against Coinbase was not entirely unforeseen. This blog covers the potential signals using the Unstructured Data Terminal.

Traders utilize sentiment factors from both Twitter and StockTwits to confirm social sentiment or identify high message volume securities. Using sentiment from two unique sources provides a strong signal. A sample long only portfolio with no overnight position yields cumulative returns greater than 70% since the beginning of 2022.

May 24, 2023

Context Analytics has a variety metrics derived from Social Media feeds such as Twitter and StockTwits. Here we look at the simplest and most raw sentiment factor: Raw-S. Recently, Raw-S has been highly predictive of market returns at the Open. This Daily strategy using only S&P 500 stocks yields a Long/Short that has outperformed SPY by 30% since 2022.

May 18, 2023

Even on the most liquid stocks, Context Analytics’ Social Sentiment provides an edge. Using only S&P 500 constituents, this Monthly Social Sentiment Index outperforms the market by over 2.5% annually over the past 5+ years.

May 10, 2023

Fast acting information distributed through social media sites like Twitter can improve investors’ returns. Using Social Sentiment data intraday allows traders to outperform market benchmarks within minutes of information being released.

May 4, 2023

Using intraday Social Sentiment monitoring can inform traders of any changes in market conditions and help them act fast. Stocks that have extremely positive sentiment from recent Twitter conversation, outperform the market over the subsequent hours.

April 26, 2023

Context Analytics’ Social Sentiment Score, S-Score, has been a consistent predictor of excess return and underperformance over the sector average over the last 10 years.

Context Analytics daily sentiment Long/Short portfolio without overnight risk yields 80% return since the beginning of 2022. When overlayed with historical security performance statistics, that adds over 25% to its cumulative return over this period.

April 12, 2023

Companies and individuals are increasingly focused on electric vehicles (EV) to contribute to a more sustainable future. With the increased investments in the electric vehicle, which companies are most impacted? With ThemeX, investors can identify keywords and phrases to examine how trends impact a variety of companies across industries and sectors.

April 5, 2023

Context Analytics has developed its S-Factor and Activity feeds on TSX securities sourced from StockTwits messages. This aggregates StockTwits conversations on Canadian securities using our patented NLP. From a historical backtest, over the past 4+ years, the spread between TSX securities in the highest and lowest S-Score quintile yields a return of over 140%.

March 29, 2023

Context Analytics daily sentiment portfolio without overnight risk yields 75% return since the beginning of 2022, outperforming the S&P 500 which had a negative return over the same period.

March 22, 2023

In the third part of our SVB series we are going to use ThemeX to explore press releases related to SVB.

March 15, 2023

Previously, we discussed how investors could have seen the collapse of SIVB coming through regulatory filings. There were multiple red flags throughout recent 8-Ks and 10-K that pointed towards SIVB being exposed to risk. Today, we will look at how Social Sentiment created by Context Analytics played a role in capturing the dramatic shift in SIVB’s price.

March 14, 2023

With the collapse of Silicon Valley Bank, Context Analytics wanted to see if there were any warning signs in regulatory documents that could have hinted towards this event. SIVB’s (SVB Financial Group) stock price dropped 34% from market close on Wednesday, March 8th to market open on March 9th and a total of 60% overall.

March 8, 2023

Bitcoin (BTC) and Ethereum (ETH) are the two largest cryptocurrencies by market capitalization. One advantage to trading these two cryptocurrencies is the liquidity, allowing investors to be in and out of positions quickly with the ability to short the asset.

March 1, 2023

By using Context Analytics’ ThemeX search capabilities, users can create custom portfolios from its results. A search on ‘Increased Recurring Revenue’ yields a variety of securities that are grouped into a Monthly Long Only portfolio which outperforms the market by over 4.5% annually over a 10+ year sample.

February 22, 2023

Using Twitter sentiment and volume metrics in the Commodities market can enhance portfolio performance. A sample portfolio using only Context Analytics S-Factors, decreases risk while also outperforming the benchmark 80% over a 7-year period.

February 15, 2023

Context Analytics provides predictive Social Sentiment data on ETFs through its S-Factor feed. When overlayed with S-Factor Performance statistics, returns are enhanced by over 4% annually.

February 1, 2023

S-Factors enables users to dissect single stock sentiment as expressed on social media. By tracking which securities have increasing or decreasing sentiment, users can create a strategy that yields over 30% annually over the past 5 years.

January 19, 2023

Users can create a combined Sentiment factor predictive of market returns using Context Analytics Twitter and StockTwits S-Factor feeds. Using sentiment factors from two unique sources confirms the accuracy of data and provides a strong signal.

This past year, Context Analytics Social Sentiment metrics enhanced stock selection and strategy returns. A daily Long/Short trading strategy with no after-hours risk led to an annual return of more than 50% compared to the 2022 bear market. We review the performance of 2022 S-Factors and give users different ways of utilizing these unique Social Sentiment metrics.

December 21, 2022

In this blog, we explore how to utilize Context Analytics technology to stay on top of key developments and trends in ESG in 2023.

December 14, 2022

Context Analytics looks at a variety of derivative metrics from its Social Sentiment feed to analyze prediction power. Here, we look at the daily change in sentiment score paired with its Twitter buzz. On a large universe, this factor demonstrates its monotonic relationship with 1-day price returns.

December 6, 2022

Examples and descriptions of some of the social sentiment widgets we have created for our partners.

November 29, 2022

With the price of used cars recently declining, which companies will be most greatly impacted? With Context Analytics (CA) ThemeX, investors can pinpoint key words and phrases to see how trends can affect an array of companies across multiple sectors and industries.

November 22, 2022

Twitter’s new ‘Twitter Blue’ product allows users to pay for verification to gain more influence on the platform. This does not affect Context Analytics’ Social Sentiment metrics because ‘Verified’ is not a factor in our Account Rating Algorithm.

November 14, 2022

The collapse of FTX sent shockwaves around the Crypto world. Context Analytics’ tools were able to identify red flags in the company hours before the collapse of FTX and FTX token.

November 8, 2022

Using the Unstructured Data Terminal (UDT), users can discover insights in textual data sourced from Earnings Calls, Regulatory Filings, and Social Media. We explore findings on MNST earnings from the previous week.

October 31, 2022

With current market volatility, we are frequently asked how our data is performing. This blog goes over charts YTD Open-To-Close return of common stocks with an S-Score > 2 or S-Score <-2 prior to Market Open.

October 24, 2022

Our S-Score is predictive across all universes and market caps. For daily holding periods, a strategy with a universe of all Market Caps and only S&P 500 stocks both outperform the overall market.

October 19, 2022

Our S-Score creates a once a day Long/Short trading strategy that outperforms the market by over 30% (with minimal risk) since the start of 2020. With messages sourced from Twitter and StockTwits, these two distinct data feeds unveil hidden alpha from the social masses.

October 12, 2022

Social media informs corporate decisions by studying the decision of firm management to withdraw an announced merger. Findings imply that social media is not a sideshow, but an important aspect of firm information environment.

October 10, 2022

Using SMA Classifications feed we created a Daily Long/Short strategy that has outperformed SPY by over 4.5% annually over the past 5 years.

October 3, 2022

Due to climate and social challenges, companies have begun shifting priorities to include Environmental, Social and Governance (ESG) initiatives into their business practices. ESG reports inform investors on how companies are implementing ESG policies.

September 27, 2022

A few hours ago it was announced that there was a leak in the Nord Stream Gas Pipeline. With our Unstructured Data Terminal, we quickly found which companies could be impacted by this event.

September 19, 2022

Using SMA’s Social Sentiment to tilt weights of S&P 500 constituents monthly enhances index performance by over 1.5% annually.

September 7, 2022

We explore how SMA’s unique factors from SEC Regulatory Filings can be predictive of quarterly price returns. Document length and Sentiment are calculated and compared to historical baselines to identify alpha.

In this video we demonstrate how easy-to-use and powerful the ThemeX tool is on the Unstructured Data Terminal. We use ThemeX to search filings, transcripts and social media for macro insights on the impact of a recession.

August 24, 2022

As a follow up to our previous blog we now explore how quantifying textual data from the Q&A portion of Earnings Call Transcripts with sentiment analysis can provide insights to future stock price movement over quarterly holding periods.

August 9, 2022

Earnings calls are one of the most important communications with investors.. SMA applies our patented sentiment metrics to earnings calls to make the analyzation process more efficient. We find excess returns with very positive sentiment when isolating the Q&A section.

August 3, 2022

A high volatility of sentiment on Twitter indicates potential uncertainty from investors on the direction of securities. An aggregate volatility calculates the uncertainty of the market in general. Since the Covid-19 pandemic, the aggregate volatility is helpful in predicting the general market direction.

July 28, 2022

A week look-back of the S-Volume factor identifies securities that are hot topics on twitter. Securities with a high aggregate S-Volume score consistently outperforms those with a low S-Volume score. Being talked about matters.

July 18, 2022

SMA is proud to announce that in Partnership with S&P Global we are releasing a full set of ESG documents as part of GMRF. In this blog, we introduce the exclusive library of ESG Documents and the content within them.

June 21, 2022

Stock prices tend to follow the follow the movement of their sentiment on twitter, especially when it contradicts the overnight pricing momentum. Adding sentiment to a momentum trading strategy improved the annualized return of the long position by 12% and the short position by 8%.

May 10, 2022

In our first video blog we explain how our S-Factor feed uses the Twitter firehose to build trading signals, dashboards and widgets to help investors increase alpha.

April 12, 2022

This blog discusses the launch of SMA's TSX Asset class and alpha generated from this data set

March 21, 2022

In this blog we discuss the impact that the war in Ukraine has on EDGAR and Global Filings. We analyze the impact using the ThemeX feature on our newly released Unstructured Data Terminal.

November 1, 2021

In this blog we explore the returns of word count and sentiment within global annual reports using Global Machine Readable Filings

September 14, 2021

In this blog, we test the predictability of SMA's S-Score data on price movement during earnings season

July 28, 2021

This blog demonstrates the offerings and unique features of Global Machine Readable Filings. Global Machine Readable Filings is the first product to provide parsed textual data of over 200 Countries Company Annual Reports, Quarterly Report, Semi-Annual and Financial Supplements across ~1.6M documents.

June 21, 2021

This blog is about using SMA's S-Factors to aggregate and create long-term Social Media signals utilized for a Monthly Trading Strategy.

In this blog we analyze the conversations of Rare Earth Metals within SEC Edgar Filings, using SMA’s complex topic modeling in the new Machine Readable Filings (MRF).

May 17, 2021

In this blog we explore the return characteristics of special acquisition corps using metrics from our new SPACs as an Asset Class data feed.

May 4, 2021

Textual Consistency Matters and the Market Rewards It: Firms with the most year-over-year textual similarity outperformed those with the least similarity by 4.18% in the MD&A section and by 5.26% in the Risk Factors section annually after accounting for commonly used risk strategies.

May 1, 2021

In the wake of the recent GameStop (GME) short squeeze, we received a lot of inbound questions on social media’s predictive power for short squeezes. This blog explores subsequent return characteristics in the SMA Short Squeeze data feed.

March 31, 2021

10-Q & 10-K filings are a vital source of information, but their length and complexity may result in investors overlooking important details. In the latest report, the Quantamental Research group uses Natural Language Processing to identify companies that have made significant changes to the “Risk Factors” section of their corporate filings.

February 22, 2021

Since the now famous GameStop (GME) short squeeze we have received inquiries about Twitter’s ability to identify short squeezes. This blogs introduces SMA's Short Squeeze Data Feed, a product that helps identify stocks prior to their squeeze.

February 22, 2021

February 2, 2021

In this blog we look at how SMA's Machine Readable Filings (MRF) product improves on raw EDGAR downloads. MRF offers a concise and efficient way to analyze text in corporate filings.

January 14, 2021

This paper is an analysis of the Machine Readable Filings (MRF) 8-K dataset to predict future U.S. Equity returns. SMA partnered with S&P Global Market Intelligence to provide textual data in U.S. SEC EDGAR filings broken down by heading with text underneath (i.e. Parts, Items). We look at the predictive power of the 8-K data set on the Document as well as the Item levels, including Word Count and Sentiment fields.

January 4, 2021

This blog will explore the predictive nature of our Futures Twitter based sentiment factors by tracking Futures contracts' Settle-to-Settle performance based on SMA's sentiment metrics.

December 1, 2020

In this blog we will be illustrating the power of SMA’s complex topic modeling in the new Machine Readable Filings (MRF) product by identifying companies in thematic investing. This blog uses 'Drones' as an example topic.

October 26, 2020

This blog is an analysis of the 8-K filings from SMA's Machine Readable Filings (MRF) dataset. We look at the predictive power of the sentiment values of the 8-K filings towards the companies' future equity returns.

October 13, 2020

In this blog, we look at a Crypto Currency broad market indicator built with SMA sentiment data that is predictive of future Bitcoin prices. We call this indicator the Crypto Market Score (CMS).

This blog is an analysis of the ESG Topic Model on the Machine Readable Filings (MRF) dataset. SMA partnered with S&P Global Market Intelligence to provide textual data in U.S. SEC EDGAR filings broken down by heading with text underneath (i.e. Parts, Items). Utilizing MRF and SMA's Topic Modeling technology, we analyze the breadth of who's mentioning ESG in their filings and the depth of the mentions.

July 20, 2020

In this blog, we look at how SMA captures the most relevant and indicative information for each of the securities we track on Twitter - Topic Modeling, and Account Filtering.

This blog is an analysis of the Machine Readable Filings (MRF) dataset to predict future U.S. Equity returns. SMA partnered with S&P Global Market Intelligence to provide textual data in U.S. SEC EDGAR filings broken down by heading with text underneath (i.e. Parts, Items). In this blog, we look at the predictive power of the data set on the Document, as well as the Item levels.

June 29, 2020

This paper is an analysis of the Machine Readable Filings (MRF) dataset to predict future U.S. Equity returns. SMA partnered with S&P Global Market Intelligence to provide textual data in U.S. SEC EDGAR filings broken down by heading with text underneath (i.e. Parts, Items). We look at the predictive power of the data set on the Document, as well as the Item levels.

This blog explores the predictive nature of metrics on regulatory filings using SMA patented NLP and machine learning from the recently release Machine Readable Filings (MRF) Product.

S&P Global and Social Market Analytics launched Machine Readable Filings (MRF), a sophisticated new data offering which applies Parsing and Natural Language Processing to generate machine readable text extracted from SEC Regulatory Filings.

March 30, 2020

This paper discusses the analysis of U.S. Equity Returns using Machine Readable Filings (MRF) word counts. It focuses on change in word counts in 10-Ks and 10-Qs as it is builds on existing academic research Lazy Prices.

March 16, 2020

In this blog we look at SMA Sentiment Score's performance over the past few weeks, amid the recent market volatility due to COVID-19.

January 16, 2020

This blog goes over the predictive power of SMA's S-Score, a statistical Z-Score calculation on the current sentiment. The analysis shows that the more significant the S-Score, the more extreme the subsequent returns.

This blog post highlights research done on an excellent research platform My Data Outlet (MDO). MDO specializes in integrating financial data into R. They offer an API to access financial data, allowing for a single access point for extracting data. The research provides a great illustration of the predictive power of SMA's metrics.

September 4, 2019

This blog answers the question – “Do SMA's Machine Learning algorithms really add value to the NLP process?”. Answer -> Yes.

August 30, 2019

SMA's Joe Gits with Kai Ryssdal on NPR Marketplace, talking about market reactions to the presidents's tweets.

August 26, 2019

This piece shows the performance of SMA’s sentiment data in the volatile market of 2019, illustrated by returns and Sharpe/Sortino ratios.

Coin Metrics and SMA announced today a partnership to incorporate SMA’s Crypto Currency Data Feed into the Coin Metrics Market Data Platform.

Coin Metrics is incorporating SMA's cryptocurrency data feed into its market data platform.

May 31, 2019

The CME Group had SMA into speak to the Data and Marketing Teams about AI, Machine Learning, and NLP across Finance and Futures and Options

Social Market Analytics has two U.S patents developed "to prevent just this kind of abuse."

RCM-X is partnering with SMA to incorporate SMA's Cryptocurrency Data Feed into the logic of RCM-X's advanced order types and technologies.

SMA aggregates the intentions of professional investors as expressed on Twitter. We identify these professional investors using our proprietary twelve factor ranking system. One factor is the forward accuracy of Twitter accounts. If a Twitter account is tweeting bullishly based on our patented NLP process and the security subsequently moves higher over specified periods that account is deemed to be accurate over that period. We found significant variability in account accuracy for supposed professional investors.

IHS Markit recently added SMA's LSE 1000 Equity S-Factor Feed to their data offerings. In conjunction with the launch IHS Markit authored a research paper exploring the predictive nature of the SMA S-Factor data on LSE equity securities.

March 11, 2019

IHS Markit recently added SMA’s LSE 1000 Equity S-Factor Feed to their data offerings. In conjunction with the launch IHS Markit authored a research paper exploring the predictive nature of the SMA S-Factor data on LSE equity securities.

January 22, 2019

SMA aggregates the intentions of professional investors as expressed on Twitter. We apply our patented filtering and natural language processing(NLP) to Tweets to proactively select Twitter accounts to use in our predictive metrics. From the perspective of 2018 market performance, this blog answers two questions we get regularly: How would your data perform in a bear market? And what is the benefit of your NLP and account ratings systems?

In June of 2017 SMA launched a weekly re-balanced large cap sentiment based index (SMLCW). This index is comprised of twenty-five stocks with the highest average Twitter sentiment over the prior week selected and re-balanced Friday afternoons from the CBOE Large Cap 450 Index. This blog takes a look at SMLCW's significant performance in 2018, a 0.87% gain compared to a 8.4% loss on the S&P 500 Index.

December 11, 2018

Social Market Analytics (SMA) tracks real-time sentiment on equities, commodities, currencies, ETF’s and crypto currencies. SMA has the most powerful and customizable Alerting API combining Twitter sentiment and pricing metrics. Users receive custom real-time sentiment alerts on instruments in their watch list.

November 28, 2018

SMA launched the SMLCW index in partnership with the CBOE two years ago. This index is re-balanced weekly and comprised of the twenty-five securities selected from the CBOE large cap universe with the highest average S-Score over the prior week. This blog takes a look at its performance in 2018, a tough year for most investment strategies.

November 21, 2018

SMA's NLP is unique because of our proprietary processes that tag sentiment weights based on the language used in finance per asset class. Recently, we did as study on using SMA signals to create a Long Short trading strategy using Natural Gas futures. The results show a significant outperformance from Natural Gas prices.

November 13, 2018

SMA is happy to participate in the "Using artificial intelligence, machine learning & big data for QIS investing panel discussion" in London

November 8, 2018

The CME Group has partnered with Social Market Analytics, Inc. (SMA) on the CME Active Trader platform to provide predictive sentiment data analytics across six asset classes and thirty-six commodities. The CME Group is leveraging SMA’s Patented processing technology in machine learning and natural language processing (NLP) to provide users with new alternative sentiment data to a trader’s tool kit.

The SMLCW Index is a Long Only Index that has outperformed since it was released and has continues to outperform in the recent market volatility and sell-off. In the chart below the S&P500 is flat for the year and SMLCW is up nearly 5% YTD.

October 18, 2018

With the SMA team continuously expanding and improving the technology, SMA recently received a second patent as an extension of the original patent. The first patent was on the three-component system for extraction, evaluation and publication of metrics on social media feeds. SMA now has two granted U.S. Patents.

October 10, 2018

SMA covers the Top 1000 securities on LSE ranked by market cap. This blog is about the predictive nature of our LSE security universe. We calculate our custom metrics on the top 1000 market cap securities listed on the LSE. Our LSE data starts on 1/1/2016. The quintile analysis confirm the predictive nature of dataset in LSE data. The spread between the top and bottom quintiles is 10% annualized and sharpe and sortino numbers show a high return to risk ratio.

September 26, 2018

Social Market Analytics (SMA) publishes real time Twitter based sentiment for nearly 350 crypto currencies including Bitcoin. In this post we will review a sentiment-based Z-Score strategy to generate profitable trades for Bitcoin.

September 24, 2018

Social Market Analytics (SMA) data is live on the CME Active Trader Website. Real-time sentiment and indicative Twitter volume is can be tracked used by traders to generate new ideas.

September 20, 2018

This blog explores a trading system using the SMA Twitter based sentiment data to trade a basket of Forex with two strategies: Sentiment RSI, and S-Score Based Currency Selection Model.

August 22, 2018

SMA is excited to announce a partnership with the Chicago Mercantile Exchange to provide real-time Twitter based sentiment for their active trader website, giving commodity traders instant real-time access to Twitter based sentiment metrics.

June 15, 2018

This paper revisits the social media indicators IHS Markit & SMA introduced back in 2014. It reviews factor performance since the model’s inception, with focus on a key predictive factor, S-Score™. S-Score™ interactions with short-term price momentum and short interest factors are also analyzed. Furthermore, it also considers the application of sentiment aggregated at the market level.

May 7, 2018

SMA CEO Joe Gits speaks at the Barclays Risk Premia Forums in Singapore on May 7th and Hong Kong on May 9th

May 4, 2018

The Benzinga Global Fintech Awards are a yearly showcase of the greatest advances in fintech from leaders and visionaries in the worlds of finance and technology. This year, executives, developers and innovators from the likes of Facebook, Amazon, IBM, JPMorgan, TD Ameritrade, TradeStation, Fidelity, Zelle and so many more attending the Oscars of Fintech.

The SMA Practicum Group at University of Illinois worked with RCM Capital in the spring of 2018 to develop a Bitcoin trading strategy combining price momentum with sentiment.

May 3, 2018

SMA takes a look at sentiment's impact on the cryptocurrency market in a practicum with the MSFE students from the University of Illinois in the spring of 2018. The SMA Practicum Group worked with RCM Capital to develop a Bitcoin trading strategy combining price momentum with sentiment.

March 29, 2018

Louise Robbins bought shares in an exchange-traded fund last Friday afternoon as markets fell, knowing that she had enough money in her Vanguard Group settlement fund to pay for the trade.

February 27, 2018

SMA creates actionable intelligence from social media data by filtering out the noise to deliver clean data on sentiment for financial markets. More specifically, it produces a family of metrics, called S-Factors™, designed to capture the signature of financial markets sentiment.

February 20, 2018

SMA has been creating security level sentiment metrics for six years. This blog will discuss the application of sentiment to a long only 50 stock, re balanced annually, index.

January 8, 2018

This blog shows SMA's sentiment data performance in 2017, illustrated with tables of Open to Close performance of securities with the aid of sentiment scores.

January 8, 2018

Trading volume predictors are part of a continuous iterative research process at most firms. Trading volume depends on multiple factors such as the market activity, political events, global unrest and human behavior. This paper explores the use of social media signals to predict trading volume by using linear regression testing and correlation analysis.

January 2, 2018

SMA's Crypto Currency Data Feed has gone live covering +270 Digital Assets, Exchanges, and Futures. The CC Data Set has the same monotonic profile of all SMA Asset Classes and is being used in trading by Market Makers and for Portfolio Management

December 5, 2017

SMA is celebrating six years of out-of-sample data in US Equities. This data is unique in that it is a true representation of the Twitter conversation at each historical point-in-time.

December 4, 2017

The SMA Practicum Group at University of Illinois, during the fall semester of 2017, created a new sentiment enhanced index, the SMA50 Index. The index measures the aggregate performance of stocks with high levels of crowd sourced commentary and high market liquidity. This piece explains the construction of the index, as well as analyzes its performance.

December 1, 2017

SMA has expanded into EMEA with it first offering. SMA is live an in production with clients covering the FTSE1000. Similar to U.S. Equities, SMA offers the FTSE data in across four feeds: S-Factor™, Activity, Tweet Level, and Lexical.

“Twitter is clearly taking the lead as the home for discussions related to new monetary technologies,” Social Market Analytics‘ Joe Gits declares to Jared Podnos. And it does seem to be the case.

August 1, 2017

This is an extension to the Research Paper titled “Signal Processing: Social Media Sentiment” published by the Deutsche Bank Quantitative Research Group. This extension expands on the technical indicators and range strategy concepts of the original paper and finds that it is advantageous to incorporate technical indicators that capture sentiment momentum and sentiment volume.

July 17, 2017

Deutsche Bank Quantitative Research Team released a full research report exclusively on SMA's sentiment data. This report independently verifies the predictive nature of the SMA's S-Factors™.

July 6, 2017

This research explores how natural language processing techniques can be used to process qualitative data to form equity return forecasts. Specifically, it analyzes SMA Indicators provided by IHS Markit which estimate stock-level sentiment from twitter data for US equities.

July 4, 2017

Social Market Analytics, for instance, culls millions of tweets a day to give “quantitative” traders a sense of what direction a stock may be moving, said Joe Gits, the company’s chief executive. The firm is on the lookout for false leads and avoids tracking small companies with little following, known as penny stocks, he said.

JPMorgan names Social Market Analytics, Inc. (SMA) as one of the Top 43 Big Data Companies. "These new "alpha generating" data sources have become a significant source of competitive advantage for investors. J.P. Morgan predicts that analysts and portfolio managers who don't have access to these data sources will be left behind."

May 10, 2017

Traditional passive indices such as the S&P 500 use a metric such as float adjusted market cap to calculate the weights of each company in the index. This research paper talks about applying an additional sentiment layer on top of the float market cap to further adjust the weight of the stocks to enhance performance.

April 21, 2017

Joe Gits, CEO of SMA, spoke at the 34th annual CBOE Risk Management Conference. Gits spoke about SMA’s patented technology, the Social Sentiment Engine, and Twitter’s relevance in financial markets.

On April 20th 2017, discussion started on Twitter that Ocwen Financial was going to be investigated in relation to sub prime mortgage concerns. SMA's sentiment data provided a strong sell signal 40 minutes before the price drop.

March 10, 2017

This blog explores decile groupings based on SMA's S-Score™, and their corresponding cumulative subsequent returns.

February 16, 2017

Joe Gits, the chief executive of SMA, commented on the market reactions to the president's tweets.

February 2, 2017

SMA culls Twitter feeds, including posts by people in the StockTwits trading community, for positive or negative remarks on specific stocks and delivers that as a metric to its customers.

February 1, 2017

This paper looks at the performance of SMLC (SMA Large Cap Index) SMA launched partnered with CBOE back in September 2016.

January 31, 2017

T3 is far from the first company to capitalize on Trump's targeted tweet-storms, made evident by the almost instantaneous market response to his online remarks, analysts told the Los Angeles Times in mid-January. "It's in the algorithms," said Joe Gits, chief executive of Social Market Analytics. "They've done it."

January 23, 2017

This piece shows the performance of SMA's sentiment data in 2016, illustrated by returns and Sharpe/Sortino ratios.

January 19, 2017

Trump’s market moves are “getting press now because of our next president’s propensity to tweet” and Trump’s upcoming ability to actually change the business climate, Gits said. “But it really started a couple of years ago.”

January 16, 2017

The jaw-dropping speed at which certain stocks have moved in response to Donald Trump’s tweets about corporate America makes it seem as if Wall Street already was waiting for the president-elect’s words. It was.

January 13, 2017

Chicago Board Options Exchange has launched the CBOE-SMA Large-Cap Weekly Index (SMLCWSM Index), the second in a series of sentiment-based strategy benchmark indices designed to capitalize on short-term market momentum based on SMA metrics.

January 10, 2017

This paper expands on the JHU research paper (Liew & Budavari, 2016) exploring the predictive power of StockTwits based sentiment data. It is postulated that using a fine grain text analytics approach on social media posts is a better representative of the sentiment factor. This new model shows improvement in both Fama French 5 Factor Model and the model in JHU paper.

January 9, 2017

This piece explores the use of SMA data for weekly, monthly and quarterly holding periods in portfolio managements.

December 14, 2016

Even before Donald Trump went on Twitter and posted his market-cratering tweet lambasting Lockheed Martin‘s F-35 fighter jets, the company’s stock was already falling.

October 24, 2016

Now with five years of out-of-sample history, SMA created statistically significant signals with monthly and quarterly holding periods. This blog shows the use of sentiment data for monthly and quarterly holding periods, and also explores a trading system by looking at exhaustion in social media.

September 19, 2016

Since SMLC (SMA Large Cap Index) launched six weeks ago, there has been a significant increase in volatility. This piece shows how SMLC has performed during this period of increased volatility.

September 12, 2016

SMA and CBOE researchers have been working on multiple indexes, the next index (SMLCW) is a weekly rebalance portfolio based on the average sentiment of stocks during the week as measure on Friday mornings prior to the Open.

August 29, 2016

Can you trade off of Twitter? The Chicago Board Options Exchange and its partner SMA believe so.

August 25, 2016

This paper discusses the analysis of a Returns Study done on US Equities using SMA's sentiment factors in a single factor trading model environment. In a comparison to a market reference on a long only strategy, the results indicate an outperformance in returns for positive sentiment stocks and an underperformance for negative sentiment stocks. The long short strategy outperforms the market reference consistently over multiple testing periods.

August 19, 2016

On July 29, CBOE and SMA launched the CBOE SMA Large Cap Index (SMLC) which tracks the return of a hypothetical portfolio strategy based on SMA S-Scores™. It has outperformed the S&P500 over the past three weeks.

Produced in partnership with Chicago-based SMA, the CBOE-SMA Large Cap Index (or SMLC Index) formally announced Monday is being touted as the first of what is expected to be a series of sentiment-based strategy benchmark indexes that will aim to measure short-term market momentum.

June 26, 2016

The SMA Practicum Group at University of Illinois, during the Spring semester of 2016, created a new sentiment enhanced fund. The research modifies the existing S&P 500 sector tracking ETFs (SPY, XLV, and XLY) by enhancing the highest market capitalization subset of the ETFs based on social media sentiment while still passively investing in the remaining stocks of the ETFs.

June 24, 2016

SMA was able to predict Brexit by analyzing the Twitter volume of the top hashtags on this topic.

June 22, 2016

SMA's sentiment data provided another actionable signal when Twitter broke SolarCity being acquired by Tesla Motors. The investors with SMA data in their trading models were ahead of the curve, when the rest of the market was just learning of the news.

Chicago Board Options Exchange announced today that it has entered into an exclusive licensing agreement with SMA to develop a series of sentiment-based strategy benchmark indexes based on SMA’s social media metrics.

June 13, 2016

Microsoft buying LinkedIn broke on Twitter first. SMA detected this 7 minutes ahead of any news article came out.

June 8, 2016

People seem surprised that Britain voted to exit the EU. SMA with its partner the CBOE are not nearly as surprised. Russell Rhoades from the CBOE has been blogging and Tweeting with SMA data for two weeks that it looks like the Brexit is going to happen.

May 13, 2016

StockTwits is a community for active traders to share ideas enabling you to tap into the pulse of the market. This blog will focus on the deterministic nature of the StockTwits data set when aggregated into SMA S-Factors™.

April 28, 2016

This research note addresses the question: Can social media sentiment be used to predict price movements over multi-day (as opposed to intraday) holding periods? This paper attempts to answer this question by creating a trading strategy using longer-term signals derived from S-Factors™ data published by SMA.

April 20, 2016

SMA introduces two longer term signals into the metrics: Velocity and Acceleration, which capture the rapid changes in sentiment.

February 4, 2016

SMA studies the correlation between the Twitter derived sentiment on EURUSD forex pair and the correlation with the EURUSD exchange rate in December 2015. The research note explores two frequencies- 15 minutes and daily- both of which point to same trend.

February 2, 2016

SMA's chief executive, Joe Gits, talks about how Twitter sentiment can be used to interpret political election results.

January 27, 2016

SMA takes a look at the political landscape by analyzing the sentiment on the current conversation about candidates and issues.

January 24, 2016

Social media platforms have gained prominence when it comes to investing partly because traditional information sources, such as newspapers and newswires, are no longer always first with the news.

January 9, 2016

In this JHU research paper, it explores the characteristics of securities derived from social media and discovered significant power in explaining the time-series variation in daily returns.

January 8, 2016

Using their patented sentiment calculation technology and the conversations on the StockTwits, SMA identified an interesting connection between sentiment and subsequent changes in the front month Crude contracts over the last year .

January 4, 2016

This piece shows the performance of SMA’s sentiment data in 2015, illustrated by returns and Sharpe/Sortino ratios.

December 28, 2015

The SMA Practicum Group at University of Illinois, during the Fall semester of 2015, looked at ways of enhancing ETFs. This research investigates the performance of enhanced ETF portfolios by modifying the constituent weights of cap-weighted SPDR ETFs utilizing market sentiment metrics provided by SMA. Three ETFs, SPY, XLV, and XLY, are analyzed to see how the different sectors would perform with respect to market sentiment.

December 8, 2015

This blog takes a look at the performance of a sentiment strategy on the Russell 1000, using SMA's S-Scores™ and S-Volumes™.

October 27, 2015

SMA researches modifying weights of the SPDR SPY ETF based on sentiment values and examines the impact on return.

October 14, 2015

SMA analyzes the predictive power on a close to close return basis based on the S-Score™ at 2:40 pm central time - giving a lead time of 20 minutes to make changes to the portfolio/alpha model - and buy at the close price of the day. This research, in addition to the pre-market open study, illustrates that sentiment is predictive and is not overly sensitive to timing.

October 6, 2015

SMA introduces two ways to access sentiment data without programming: Excel Add-in and Sentiment Dashboard.

September 3, 2015

This blog explores the relationship between market movement and SMA's sentiment data by looking at the percentage of positive Tweets versus the percentage of negative Tweets over the last couple of weeks.

August 28, 2015

The collective 'wisdom of the crowds' on Twitter can beat Wall Street in predicting corporate earnings and helping you make smart stock trades, a new report says.

August 11, 2015

This blog lists some recent trading opportunities social media data presented. In each case activity and sentiment increased prior to the actual event.

August 4, 2015

The SMA Practicum Group at University of Illinois investigates the benefits of using sentiment measures in classifier models designed to predict next day directional movement for volatility indexes.

SMA has just completed a comprehensive analysis that shows the performance of classifier models, designed to predict next day directional movement for volatility indexes, improves by adding market sentiment measures derived from social media sources.

July 20, 2015

SMA conducts an analysis on the cumulative returns over 3 and a half years using an intraday trading strategy based on S-Score™, and compares the historical returns with the YTD returns to see how the underlying analytics have evolved over time.

July 7, 2015

This blog reviews SMA's metrics' performance, illustrated by charts that look at the full history and YTD performance of the S-Factors™ across the entire universe.

SMA's CFO Kim Gits talks about how SMA builds S-Factors™ metrics from the unfiltered Twitter fire hose.

June 2, 2015

Today's financial technology dialog is often about a word you don't usually associate with it - democracy - bringing software, data, reporting, testing and trading to the masses. And it's not just one size for everyone - its customizable too. At the FinTech Exchange 2015 Chicago event, 13 firm executives spoke during its lightning round.

Joe Gits, CEO of SMA, explains to Crain's how Twitter data is extracted and parsed to get meaningful sentiment information.

May 5, 2015

Kim Gits, CFO of SMA, talks about Millennial investors and how they will change the future of social media use in capital markets.

April 28, 2015

Twitter got a taste of its own broadcasting power today when a web crawler found and shared its earnings on the social media service nearly an hour before its intended release.

April 21, 2015

On Mar. 27, after it broke Twitter that Intel was in talk to buy Altera, SMA's S-Score™ reacted significantly before Altera's price change.

This piece studies the relationship between social media and the market momentum.

March 3, 2015

This blog explores how predictive social sentiment is for different sectors in the financial market.

February 3, 2015

This blog discusses how SMA utilizes three different kinds of Tweet scoring methods.

SMA's chief executive, Joe Gits, explains the challenges in applying data from social media to the financial market, as well as the evolution of sentiment score calculation.

January 16, 2015

This piece explains the different ways social media sentiment can be applied in multiple areas.

SMA is announced to be one of the "Best Startups of the Year" by Red Rocket.

December 18, 2014

Energy stocks dominated the EDGE reports (which illustrates the most positive and negative industries and the sentiment of all sectors) this week.

This piece covers a transaction cost analysis over SMA's open-to-close demonstration of how social media data provides a valuable addition to a trading strategy.

November 26, 2014

This blog looks at the highlights from the EDGE report in the week of Nov. 24.

November 24, 2014

This blog looks at the highlights from the EDGE report as the Q3 earnings season winds down.

October 30, 2014

SMA harnesses the power of social media signals to deliver up-to-the-minute golden nuggets of social sentiment.

October 27, 2014

SMA leverages over 2 years of its intraday sentiment factors on U.S. securities to establish evidence of trading signals born from social media, utilizing John Sweeney's Edge Ratio as a metric to validate signals derived from SMA S-Factors™.

October 24, 2014

This paper gives a third party illustration of SMA metrics in an automated trading strategy. It details how Deltix, a provider of analytics software and services, has used social media factors to create a profitable trading system.

October 23, 2014

SMA's original white paper. This piece introduces S-Factors™, a proprietary set of sentiment metrics. It also explores how they can be used to predict price movement in the capital markets.

July 30, 2014

"Twitter is great. I like it almost as much as I like Dell,” Carl Icahn, the activist investor, exclaimed when he made his debut on the social media platform last year. He now counts 190,000 followers who hang on his every tweet.

July 29, 2014

StockTwits partnered with SMA to deliver near real-time signals from Trader Conversations on its Platform.

March 7, 2014

Joe Gits, CEO & Founder at SMA speaks to Benzinga during the pre-market info segment on 03/07/14.

Markit study confirms social media sentiment measures are effective signals of future stock performance.

March 3, 2014

This research paper is an introduction to SMA's alpha-generating social media indicators from our partner at Markit.

February 17, 2014

Diane Moca reports on how social media and markets come together with mixed results.

February 5, 2014

Joe Gits, CEO of SMA, describes the process of harvesting Twitter to provide social media sentiment.

January 28, 2014

Active individual traders now have access to the same up-to-the-minute “Sentiment” signals available to NYSE Technologies and Markit data clients.

A Canadian newspaper sent out a little-seen Tweet at 8:12 a.m. ET on Monday breaking the news that BlackBerry’s (BBRY) $4.7 billion buyout had gone up in flames. Within seconds, the clients of real-time information discovery service Dataminr received an alert warning them about the news.

NYSE Technologies and SMA have announced an agreement to distribute sentiment statistics from SMA’s patent-pending social media monitoring engine through NYSE Technologies SFTI Network, and its normalized market data service, SuperFeed.

October 15, 2013

Somebody will likely tweet this story, commenting on it for better or worse. That single tweet, a drop of water, will flow into a gushing firehose of tweets — something like 400 million worldwide each day on every possible subject.

October 11, 2013

As Twitter’s flotation approaches, Wall Street analysts are building models to calculate what it might be worth – with a figure of up to $15 billion doing the rounds.

October 11, 2013

Joe Gits, founder of Chicago-based Social Media Analytics, says he expects a turnover of $60m in two years from his system. SMA measures how far sentiment is from the norm for 8,000 US equities, from tweets by 400,000 people identified as financial professionals, active traders or market influencers.

Given the mass popularity of social media, many equity market participants are jumping on the bandwagon. But in the case of hedge funds and other trading firms, it is alpha that drives the interest, not entertainment.